|

|

|

|

|

|

Overview

There are 3 reportable amount for Superannuation:

SG

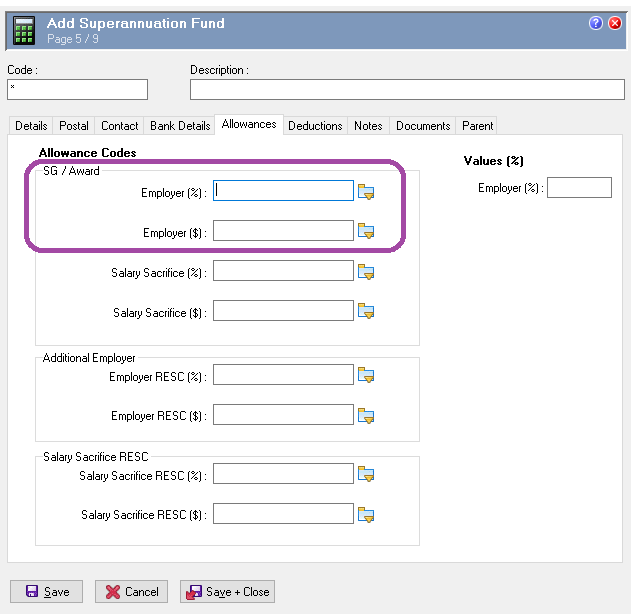

SG is derived from the allowance records linked to Employer(%) and Employer ($) fields on your Superannuation fund records, see below.

You can only populate these fields with allowances that have the following settings:

IMPORTANT: On the 1st January 2020, the Treasury Laws Amendment (2019 Tax Integrity and Other Measures No. 1) Bill 2019 changed the law to ensure that an individual’s superannuation salary sacrifice contributions cannot be used to reduce OTE or count towards a payer’s minimum superannuation guarantee contributions, if the pre-sacrifice payment was salary or wages for superannuation guarantee purposes.

In other words, no Superannuation Fund records should be using these fields anymore.

OTE

OTE is derived from allowance transaction field Total Amount from all Allowance records with Use in Super OTE = "Yes".

RESC

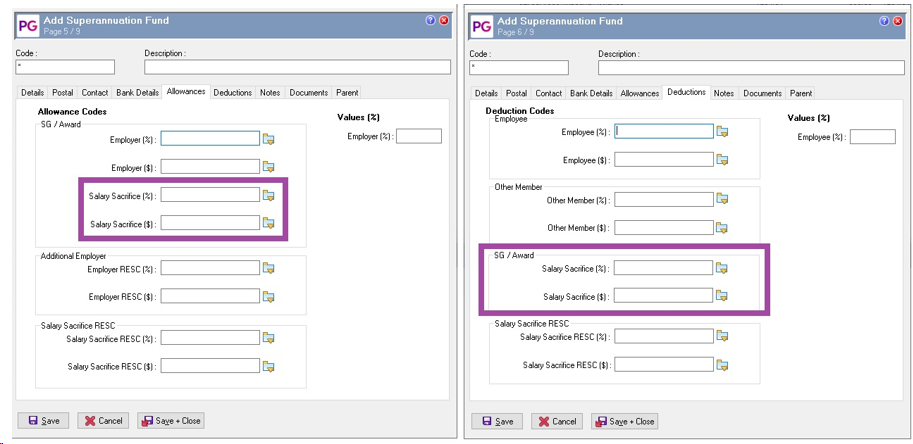

RESC is derived from the allowance and/or deduction transaction field RESC.

Note: This field is only visible in Transaction View if the allowance/deduction is linked to the "Additional Employer" or "Salary Sacrifice RESC" fields

|

|

Topic: 44817